Executive Summary

On September 16, 2025, Google introduced the Agent Payments Protocol (AP2) with backing from 60+ partners across networks, wallets, crypto, & SaaS. AP2 is an open standard that lets AI agents prove what they are authorized to buy, for how much, across cards, bank transfers, and crypto. It gives merchants, PSPs, and users a verifiable audit trail so agent-led purchases can move from demo to daily commerce.

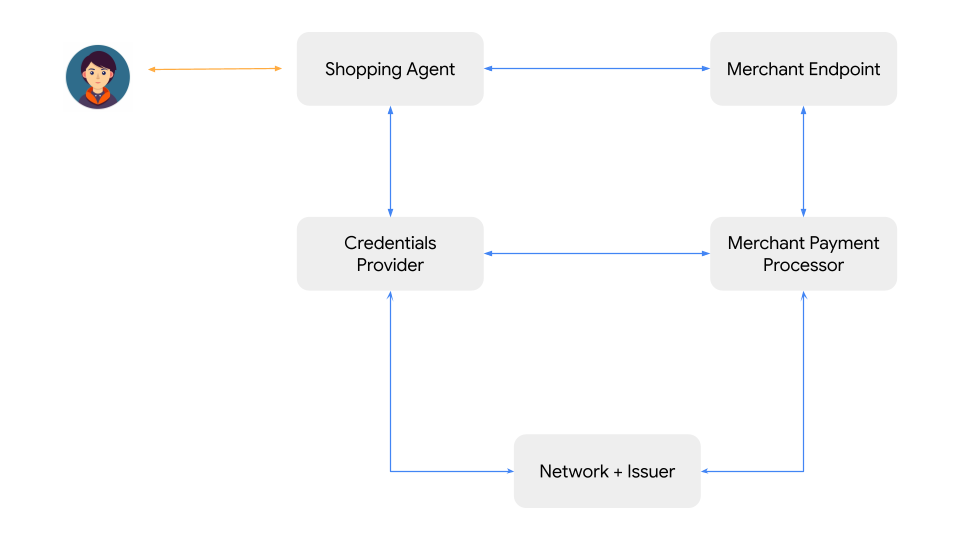

AP2’s core move replaces “click-to-buy” trust with signed Mandates: an Intent Mandate that captures the user’s instructions and limits, and a Cart Mandate that confirms the final purchase. Those Mandates are bound to the user through verifiable cryptographic credentials, creating non-repudiable evidence for disputes, fraud controls, and compliance. The spec is payment-rail agnostic, spanning cards, RTP/ACH, and stablecoins.

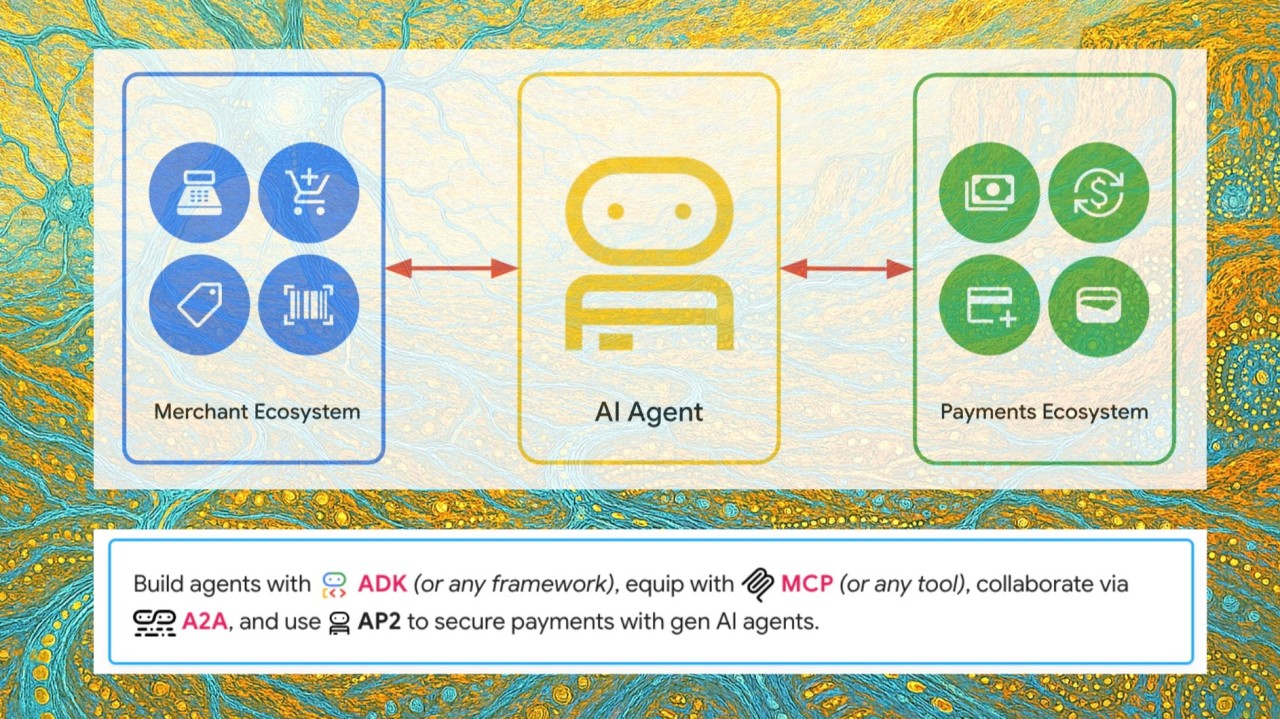

AP2 is designed to sit alongside adjacent standards. Forter’s TACP focuses on authenticating who the agent is & its relationship to a real user, while AP2 governs what the agent is allowed to buy. For crypto rails, Google & partners published the A2A x402 extension that standardizes “payment-required → payment-submitted → payment-completed” flows for on-chain settlement.

Why AP2 matters now

Agentic AI is crossing the line from chat to action. The historic blocker has been a trust gap that traditional systems cannot solve. When an autonomous agent makes a purchase, three critical questions emerge:

-

Authorization: How can merchants verify that a user actually authorized a specific agent purchase and its price limits?

-

Authenticity: How can payment providers trust that a transaction request from an agent is genuine, not malicious?

-

Accountability: When fraudulent transactions occur, how can the ecosystem determine responsibility between users, agent providers, or merchants?

AP2 provides the common cryptographic language to answer these questions, preventing the ecosystem from fragmenting into proprietary one-offs.

Industry momentum is real. Launch partners include Mastercard, American Express, JCB, Coinbase, PayPal, Salesforce, Okta, Etsy, & more. This breadth signals a push to make agent-led purchasing normal rather than novel.

How it works in practice

1) Mandate-based authorization: Replacing the “Buy Button” The protocol replaces implicit user trust in a website with explicit, verifiable consent. Users delegate with an Intent Mandate that encodes goals and guardrails—from simple requests (“Find white running shoes”) to complex delegated tasks (“Buy concert tickets when they go on sale, max $200”). The agent returns a final cart for approval, which becomes a Cart Mandate. Together they form explicit consent, not implied clicks.

2) Cryptographic audit trails Mandates are signed with verifiable credentials, producing an immutable chain from intent to payment. That evidence helps issuers, acquirers, and merchants manage risk and resolve disputes.

3) Payment-rail agnosticism The same spec spans cards, bank transfers, & crypto. For web3, the A2A x402 extension revives the spirit of HTTP 402 to standardize on-chain payment messaging between agents.

Where AP2 fits in the stack

-

A2A: the base protocol for secure agent-to-agent communication.

-

AP2: commercial vocabulary for agent-led payments using Mandates.

-

TACP (Forter): authenticates the agent & its user relationship.

-

x402: standardized crypto settlement flow for agents.

Open repos are live: AP2 main repo and the x402 extension are public under Apache 2.0, with samples and types to get started.

Early enterprise use cases

-

Smarter shopping & price watches: Pre-signed limits let agents auto-purchase when conditions are met, with clear auditability for returns & disputes.

-

Atomic travel bookings: Flight + hotel confirmed together or not at all, coordinated among multiple agents.

-

Autonomous procurement: Inventory-aware agents reorder within budget bands, or adjust SaaS licenses based on usage.

Risks to manage

-

Identity gaps without a layered approach: AP2 solves authorization. You still need an identity & trust layer like TACP to prevent bot fraud and account takeovers. Pair them.

-

Crypto volatility: If users cap price in fiat but settle on-chain, build buffers and real-time pricing checks into Mandates.

-

Regulatory evolution: Expect guidance on revocability, privacy, & dispute rights. Design for “mandate revoked” states & auditable lifecycles.

What to do next

Merchants & platforms Pilot delegated carts for sub-$200 items, integrate identity verification from day one, and join the AP2 issue queues to ensure product catalogs & promo logic map cleanly into Mandate schemas.

Payment providers & networks Offer “Mandate Verification as a Service,” plus a single AP2 integration that fans out to cards, RTP, and x402 so merchants do not rebuild per rail.

Developers Clone the repos, study ap2.types, and propose extensions for subscriptions, B2B invoicing, or multi-party escrow. Early expertise in AP2 + A2A + VCs is a durable advantage.

My Take: The Bigger Pattern

AP2 represents more than payment innovation; it is foundational infrastructure for the shift from conversational AI to agentic AI—systems that execute complex, multi-step tasks autonomously. The protocol does not make agents smarter; it makes them accountable. The fastest movers will treat Mandates like a programmable buy button and reorganize checkout, returns, and support around verifiable consent. The question is not whether to engage, but how quickly organizations can build the expertise to capitalize on this new automated economic landscape.

Six-month prediction: by Q1 2026, at least one top-50 retailer will announce an “agent-preferred” checkout that processes AP2 Mandates from third-party assistants alongside its native web & app flows, with card, RTP, & stablecoin rails live in the same integration.

Questions worth asking

-

If AP2 turns cryptographic consent into the new buy button, what other everyday interactions might require similar explicit proof of authorization?

-

When accountability becomes programmable, who gains strategic leverage: the merchants defining checkout flows, the payment networks enforcing rules, or the agent providers encoding mandates?

-

Could the same mandate logic extend beyond commerce into areas like healthcare, data sharing, or government services, where consent and auditability are equally critical?

-

What signals will tell us this trust layer has shifted from optional experiment to invisible infrastructure—much like HTTPS quietly became the default for the web?

References

[1] https://cloud.google.com/blog/products/ai-machine-learning/announcing-agents-to-payments-ap2-protocol/ Announcing Agent Payments Protocol (AP2) | Google Cloud Blog

[2] https://cloud.google.com/blog/products/ai-machine-learning/announcing-agents-to-payments-ap2-protocol Powering AI commerce with the new Agent Payments Protocol (AP2)

[3] https://techcrunch.com/2025/09/16/google-launches-new-protocol-for-agent-driven-purchases/ AP2 Announcement - TechCrunch

[4] https://www.zdnet.com/article/googles-new-open-protocol-secures-ai-agent-transactions-and-60-companies-already-support-it/ ZDNet coverage of AP2 (Agent Payments Protocol)

[5] https://github.com/forter/trusted-agentic-commerce-protocol Forter Trusted Agentic Commerce Protocol (GitHub)

[6] https://github.com/google-a2a/a2a-x402 A2A x402 Extension and Coinbase x402 Documentation

[7] https://a2a-protocol.org/latest/specification/ A2A Protocol Official Specification and References

[8] https://github.com/google-agentic-commerce/AP2 AP2 - Agent Payments Protocol (GitHub repository and docs)

[9] https://github.com/a2aproject/A2A A2A Protocol - GitHub

Appendix: AP2 Roadmap

The development and rollout of the protocol are envisioned in a phased approach, allowing the ecosystem to build, test, and adopt capabilities incrementally.

V0.1 (September 2025)

The initial specification focuses on establishing the core architecture and enabling the most common use cases. Key features include:

-

Support for pull payment methods (e.g., credit/debit cards)

-

Well-defined data payloads to support transparent accountability based on the VC framework

-

Support for human-present scenarios

-

Support for user and merchant-initiated step-up challenges

-

Detailed sequence diagram and reference implementation using A2A protocol

Deliverables

✅ AP2 specifications v0.1 (human present, pull payments) — Completed

⬜ AP2 A2A extension v0.1 — In progress

⬜ AP2 MCP server v0.1 — In progress

⬜ AP2 Python & Android SDKs v0.1 — In progress

V1.x

Subsequent versions will expand the protocol’s capabilities based on community feedback and evolving needs. Potential areas of focus include:

-

Full support for push payments and all payment methods (e.g., real-time bank transfers, e-wallets)

-

Standardized flows for recurring payments and subscriptions

-

Support for human-not-present scenarios

-

Detailed sequence diagrams for MCP-based implementations

Long-Term Vision

Looking further ahead, the protocol aims to incorporate more intelligence and flexibility, including:

-

Native support for complex, multi-merchant transaction topologies

-

Support for real-time negotiations between buyer and seller agents

A collaborative approach is essential to creating a protocol that is robust, secure, and meets the diverse needs of the ecosystem. Feedback and critique are actively sought through the GitHub repository’s issues and discussions.