Executive Summary

At Stripe Sessions 2025, the company unveiled a sweeping vision of financial infrastructure built for an era defined by artificial intelligence & programmable money. The keynote, led by William Gaybrick, President of Product & Business, showcased how Stripe is transforming from a payments processor into a comprehensive programmable financial services platform. The announcements centered around four key innovations:

-

Agentic commerce through Order Intents

-

Multi-currency programmable accounts

-

Global stablecoin integration

-

Cross-provider orchestration.

These developments portend a profound restructuring of global commerce, where autonomous agents conduct transactions, money moves instantaneously across borders & businesses gain unprecedented control over their financial operations.

How will these twin transformations in intelligence and money reshape not just commerce, but the very foundations of global economic activity?

The Dawn of Agentic Commerce

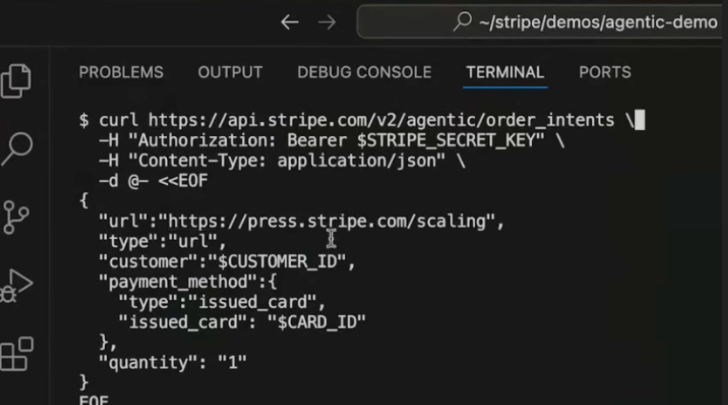

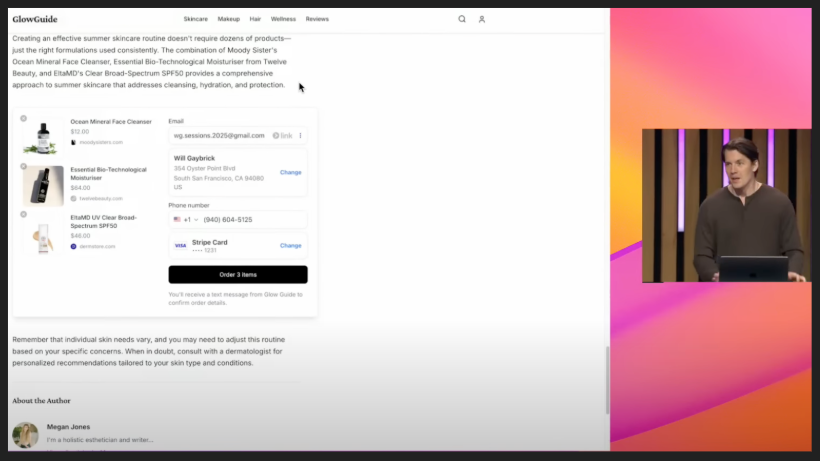

The most striking demonstration of the morning came early, as Will Gaybrick revealed “Order Intents,” a new primitive allowing AI agents to navigate the commerce layer of the internet. The technology enables autonomous agents to interpret product pages, understand pricing structures, complete checkout forms & execute purchases without human intervention.

“Agents are going to reduce friction and increase the velocity of money on the internet,” Gaybrick explained. “That means more commerce & it means we just saw new commercial models.”

The demonstration showed an agent purchasing a book through command line instructions, followed by a more complex scenario where an agent made purchases across three different e-commerce sites without the user leaving the original website. While one part of the demonstration encountered technical difficulties (a text messaging provider outage), the recorded backup showed the complete workflow in action.

This capability represents what Gaybrick called “in-situ(ation) commerce” – bringing purchase experiences directly into the context where users discover products, eliminating the friction of navigating to separate websites and completing repetitive checkout forms.

When might we see our own digital assistants handling not just information queries, but bearing the burden of transactional friction that has long characterized online commerce?

Importantly, Stripe is not pursuing this vision alone. The company announced a partnership with Visa, which recently introduced a new card specification, with Stripe serving as the exclusive launch partner for payments. This collaboration suggests that the financial infrastructure required for agent-based commerce is rapidly materializing.

The Programmable Financial Infrastructure

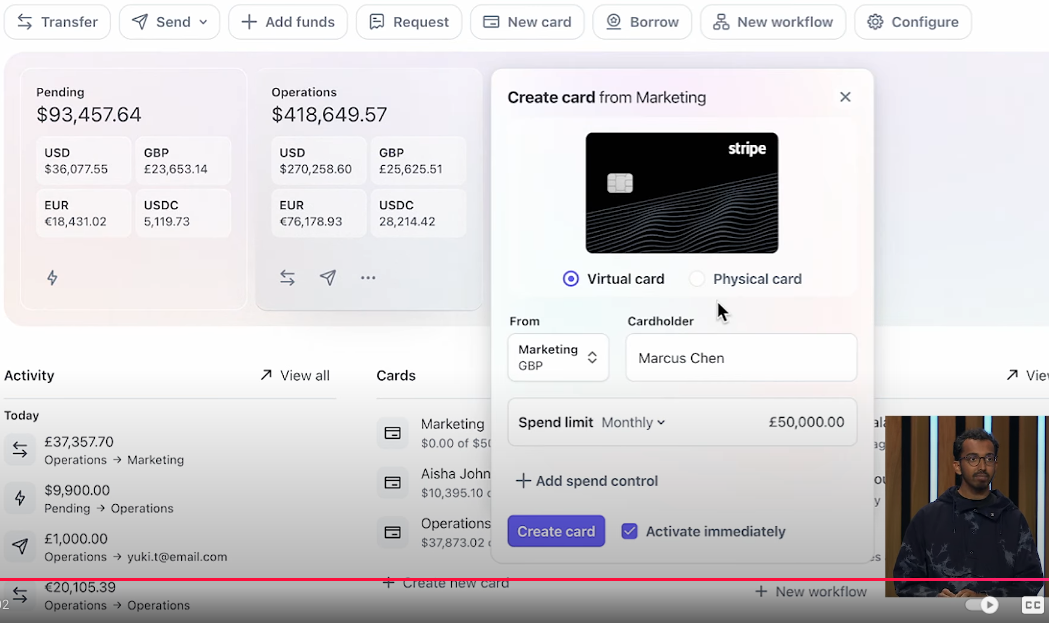

The keynote’s most transformative announcement came near its conclusion: Stripe’s expansion into comprehensive money management. The new suite includes multi-currency balances, instant foreign exchange, global payouts & stablecoin integration.

“We’re taking the first enormous step in making money finally work the way that we all know it should,” Gaybrick declared. “Money is just data, and this is how data usually works.”

The demonstrations revealed a financial dashboard that consolidated what previously required multiple banking relationships & applications. During this segment, Bharath Srivatsan showcased how users can now maintain balances in multiple currencies simultaneously, with instant conversion between them. The platform enables immediate fund transfers between accounts, instant card issuance against specific currency balances & simplified global payouts using just email addresses.

What emerges is nothing less than an alternative financial infrastructure, one built with the understanding that money should move at the speed of information – instantly, cheaply & globally.

How might businesses restructure their treasury operations when currency conversion becomes instant and borderless accounts become the norm?

Stablecoins and Global Inclusion

Perhaps the most ambitious element of Stripe’s vision involves stablecoins, which Gaybrick described as “the first truly global, actually usable, fully programmable money we’ve ever had.”

Through its acquisition of Bridge, Stripe announced the expansion of its services to 101 additional countries where traditional banking infrastructure is often unreliable. Entrepreneurs in Argentina, Vietnam, Zambia & elsewhere will be able to hold dollar-denominated stablecoin balances, receiving and sending funds across both cryptocurrency and traditional financial rails.

“So much of the world is subject to unstable currencies and unreliable financial infrastructure, and it caps the GDP of the internet,” Gaybrick noted.

To bridge the gap between cryptocurrency and traditional financial systems, Stripe is launching a global card issuing product in partnership with Visa & Leadbank. This innovation will allow developers to issue Visa cards that spend against stablecoin balances, making cryptocurrency practical for everyday commerce.

In what ways might this parallel financial system affect monetary policy, currency stability & economic sovereignty in emerging markets?

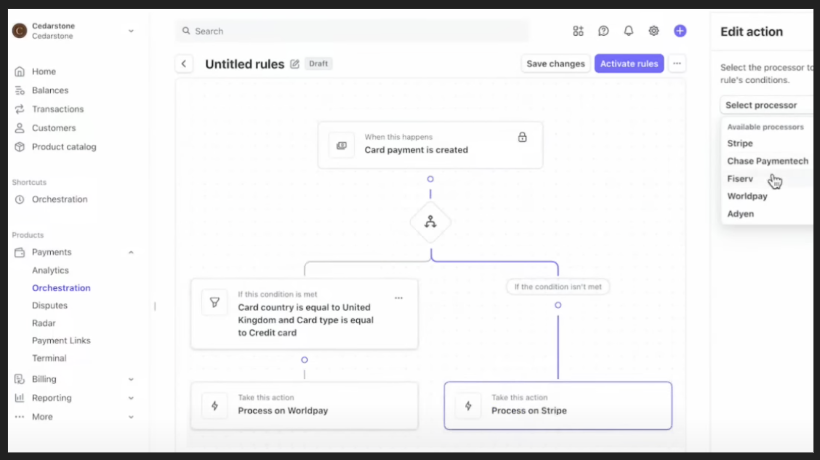

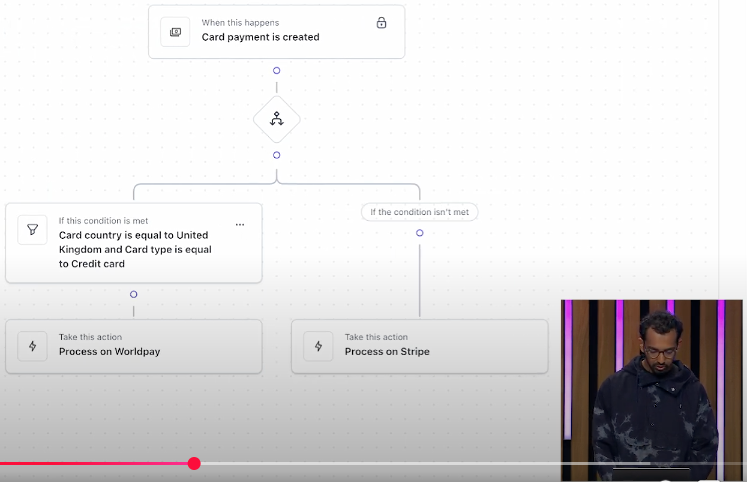

Orchestration Across Providers

Acknowledging the reality of multi-provider relationships, Stripe introduced Orchestration, a tool for managing and optimizing performance across payment service providers.

“Using Stripe with another PSP shouldn’t just be possible—it should be a first-class experience itself,” Gaybrick explained.

The demonstration showed how businesses can route transactions to different processors based on conditions like issuing bank or transaction amount. The dashboard provides analytics on performance across processors and enables optimization without requiring code changes.

“You can use orchestration even if you don’t process payments with Stripe at all,” Gaybrick emphasized, highlighting Stripe’s commitment to an open ecosystem.

When financial services become fully modular and interoperable, what new efficiencies might emerge that were previously impossible in a fragmented system?

AI-Powered Payments Intelligence

The keynote revealed how artificial intelligence is transforming payment processing through three significant updates:

-

Authorization Boost: An AI system that updates cards and tokens, routes transactions across networks & determines when and how to retry failed payments, increasing authorization rates by 2.2% on average.

-

Radar Expansion: Stripe’s fraud prevention product now covers ACH & SEPA payments with specialized AI models, reducing fraud by up to 42% for early adopters.

-

Smart Disputes: An AI tool that selects which disputes to fight and handles the process, compiling evidence automatically. Early adopters have recovered 13% more chargebacks.

Underpinning these advancements is the Stripe Payments Foundation Model, which the company described as “the world’s first foundation model built for payments.” Trained on tens of billions of transactions, the model uses self-supervised learning to generate nuanced representations of every charge, capturing hundreds of subtle signals that no human or previous model could track on their own.

The early results have been remarkable. Stripe had previously invested heavily in fighting card testing attacks, gradually reducing them by 80% over two years through traditional methods. By deploying their new foundation model, their detection rate for attacks on large users jumped from 59% to 97% nearly instantaneously, demonstrating a 64% improvement overnight.

What profound shifts in business models become possible when payment intelligence and security cease to be burdensome costs and instead become strategic advantages?

The Extensible Platform

Two new primitives, Workflows and Scripts, transform Stripe into a programmable platform that adapts to specific business requirements.

Workflows provides a visual builder for creating multi-step processes that orchestrate across Stripe products without writing code. The demonstration showed a workflow automatically converting a free trial user to a paid subscription upon reaching a usage threshold.

Scripts allows businesses to customize how Stripe itself works, changing core functionality like discount logic to match specific business rules. The demonstration showed a volume-based discount rule being deployed into Stripe’s engine with a few clicks.

“If Workflows define how Stripe products work together, then Scripts let you change how Stripe works under the hood,” explained Vic, who presented this section of the keynote.

In what ways might these capabilities reduce the technical debt that accumulates when payment and financial systems cannot evolve as quickly as business models?

Stripe as a Business Network

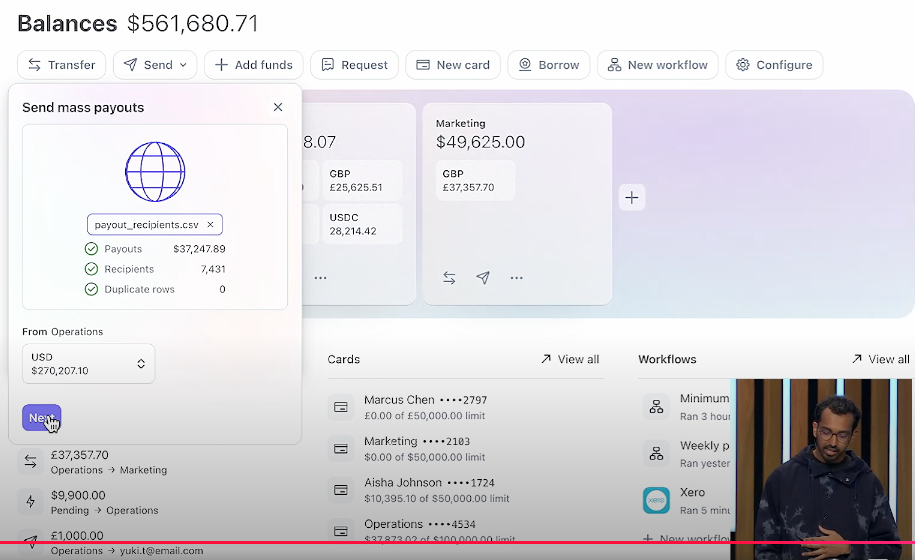

With the introduction of Stripe Profiles, the company is making its network effects more explicit. Profiles serve as a business’s identity on the Stripe network, enabling faster transactions between companies that use Stripe.

The demonstration showed how a business could invoice another Stripe user with minimal data entry & how the recipient could pay instantly using their Stripe balance. This reduces transaction costs and settlement times compared to traditional invoicing and payment flows.

A new “Stripe Verified” credential will provide additional trust within the network and streamline compliance management for growing businesses.

How might this business-to-business network challenge traditional banking relationships and reshape commerce between companies?

Expanding the Stripe Ecosystem

The keynote highlighted numerous additional product launches that enhance Stripe’s growing ecosystem:

-

Managed Payments, a new merchant of record offering coming this summer that will handle global taxes, fraud prevention, dispute management, fulfillment & more on behalf of businesses.

-

One-click Klarna payments will soon be available on Link, reducing friction for first-time users of the buy now, pay later service.

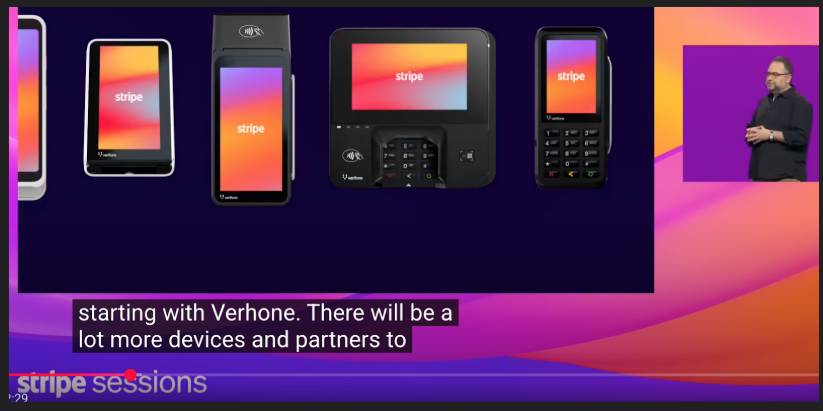

-

Terminal can now be used with third-party hardware, starting with Verifone & through a partnership with Freedom Pay, businesses can access over 1,000 point-of-sale systems.

-

Stripe Tax is now available in 102 countries, up from 57 last year & now automates the entire tax lifecycle from monitoring and registering to collecting and filing.

-

Global Payouts, which allows businesses to pay customers, contractors & other third parties with just an email address.

These enhancements, along with dozens of others announced at Sessions, demonstrate Stripe’s continued expansion beyond core payment processing into a comprehensive financial infrastructure provider.

What opportunities for innovation emerge when businesses no longer need to build these capabilities themselves?

Implications for the Global Economy

The breadth of Stripe’s announcements suggests a comprehensive reimagining of financial infrastructure for the digital age. Several themes emerged that merit consideration:

-

The convergence of AI and finance: The integration of autonomous agents into commerce represents a fundamental shift in how transactions occur. The Payments Foundation Model recognizes patterns in billions of transactions that would be impossible for specialized systems to detect. The reduction in friction could significantly increase commercial velocity.

-

The parallel financial system: Stripe’s money management suite, particularly its stablecoin integration, represents an alternative financial infrastructure that operates alongside traditional banking. This parallel system offers speed, borderless operation & programmability that traditional finance struggles to match.

-

Global financial inclusion: The expansion to 101 new countries through stablecoin accounts could provide stable financial services to entrepreneurs in regions with volatile currencies and underdeveloped banking systems.

-

Programmable commerce: The ability to customize financial workflows and logic enables businesses to align their financial operations precisely with their business models, potentially reducing the gap between commercial innovation and financial capabilities.

What economic structures might evolve when the cost of every financial transaction approaches zero and the friction of cross-border commerce disappears?

Conclusion

Gaybrick closed the keynote by highlighting the remarkable growth of businesses using Stripe: “Your revenue on Stripe is growing seven times faster than the S&P 500.”

The message was pretty clear – we stand @ the threshold of a profound transformation in how commerce functions. Stripe’s vision combines artificial intelligence & programmable money into a new infrastructure for global economic activity.

“The next decade of global economic growth will be shaped disproportionately by what each of you does, by what we can do together,” Gaybrick concluded.

In an age where technology reshapes every industry, these developments suggest that the very infrastructure of commerce itself is undergoing a fundamental reconstruction. The twin transformations in intelligence & money may well redefine not just how we pay, but how economic value flows throughout the global system.

When the means of exchange itself becomes as programmable as information, what new forms of commerce might we witness & who will be their architects?

Resources:

docs.stripe.com/disputes/smart-disputes

docs.stripe.com/billing/scripts

docs.stripe.com/payments/managed-payments